Have you ever sat in front of someone when you are trying to obtain credit and they tell you your FICO Score? Where do lenders get a FICO Score? What does that number mean and how do the credit bureaus arrive at it?

A FICO score is a 3 digit number that is based on a scoring system that analyzes your credit history. The higher your score is, statistically, the more likely you are to repay your debts. Lenders use this score to determine your eligibility for credit and how much and what terms you can borrow the money at. A FICO credit score is a moving number that is updated every 30 days on the three major credit bureaus and it is based on several factors.

What Is A FICO Score?

A FICO credit score is the number that determines your credit risk, based on your credit data that has been collected over time. A credit score helps lenders evaluate your personal credit profile. It also influences the type of credit that is made available to you. A FICO score will be used in making loan and credit card decisions, interest rates, credit limits, loan terms and more.

When you get your free annual credit report from the three reporting bureaus it typically does not include your FICO score. There has been a lot of confusion over this because VantageScore, FICO’s competitor, will give you a free score. But VantageScore will not be the same as FICO. And most banks do not use the VantageScore in making their decision. If you want to see your FICO score you will have to ask your lender or go to MyFICO and request it.

A Brief History of the FICO Score

Over thirty years ago, the Fair Isaac Corporation (FICO) started providing FICO Scores. This was to provide an industry-standard for scoring someone’s creditworthiness that was fair to both the lenders and the consumers.

Before the first FICO score, there were many different scores. Today, over 90% of lenders use a FICO score when making lending decisions.

Why Lenders Use A FICO Score

Lenders establish guidelines when creating a loan product for their customers. One of the first guidelines lenders will establish is the minimum credit score they will accept from a borrower who is looking to get a loan.

As an example, John wants to borrow $50,000 to purchase a new automobile. Lenders establish guidelines such as a minimum credit score requirement.

- Lender A requires that you have a minimum credit score of 680 to borrow money for your purchase.

- Lender B may require a minimum credit score of 620 to borrow the money and allows for other positive attributes to help the borrower qualify.

Each lender makes their own guidelines based on the type of lending they want to participate in.

FICO Scores today are used by creditors to assess an individual’s credit risk. 90% of top lenders will only use a FICO Score to determine eligibility. It is the most widely used credit score by lenders. FICO Credit Scores play a significant role in billions of lending decisions every single year.

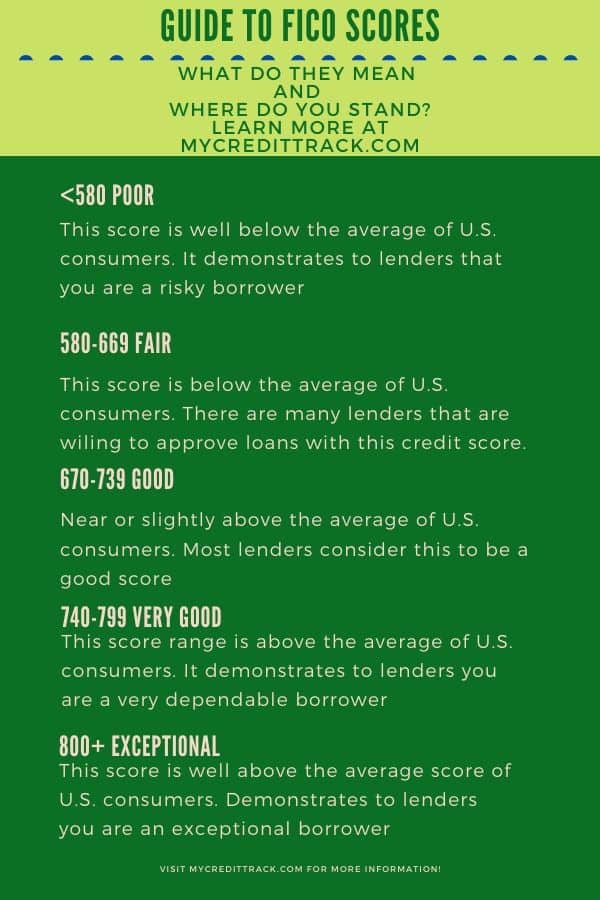

What Is A Good FICO Score?

Each lender determines what they consider a good credit score. In general, a 640 score is considered fair and used in many lender’s guidelines. Scores over 670 is considered good and over 800 is considered exceptional. The higher your score, the more lenders will be willing to lend to you. History and statistical data has shown that people with a higher credit score are at less risk for default.

This chart provides the ranges for FICO Scores found across the United States and its consumers. Each lender has its own credit risk guidelines and there are typically lenders who work with most scores. This chart can serve as a general rule of thumb for what each particular FICO Score represents.

Why Are FICO Scores Important?

FICO Scores are important to the lenders because it allows them to understand their risk and the borrower better. Years of data have gone into calculating the FICO Scores.

It is important to understand your score and know where you stand when you go to borrow money from a lender. In addition, working towards a higher score can help you in the negotiation process when looking for a loan.

FICO Scores allow you to gain access to funds that you would not normally be able to have at your disposal for making purchases such as automobiles, homes and even funding an education. They are an important tool for you and lenders to understand the impact of your decisions when it comes to managing your debt.

How Is My FICO Score Calculated?

- Payment history: 35%

- Outstanding debts: 30%

- Length of your credit history: 15%

- Types of credit you’ve used: 10%

- Amount of new credit: 10%

There are 5 factors that affect your credit score. Credit scoring models want to see that you manage all different types of credit lines with on-time payments and low credit balances. There are 4 types of credit. Credit cards, known as revolving credit, installment loans, mortgages and auto loans. You want to have a good mix of all of them to help keep your credit score as high as possible. Having all of the types of credit is not necessary to have a high score though.

FICO Score vs VantageScore

Not all credit scores are FICO Scores. FICO Scores typically have been the industry standard for determining a person’s credit risk. Other credit scores can be very different from FICO Scores—sometimes by as much as 100 points invariance!

FICO and VantageScore are two popular credit scoring methods. They each use different algorithms to calculate credit scores.

The VantageScore credit scoring model was first introduced in 2006 by the three reporting bureaus. VantageScore was developed in a joint effort by Equifax, Experian, and TransUnion/ It was used to create a more accurate credit model and to offer consistent credit scoring. Your VantageScore is determined by evaluating your credit report, weighted as follows:

VantageScore Model

- Recent credit amount: 30%

- Payment history: 28%

- Credit utilization: 23%

- Account balances size: 9%

- Depth of the consumer’s credit: 9%

- Amount of available credit: 1%

FICO Score Model

- Payment history: 35%

- Outstanding debts: 30%

- Length of your credit history: 15%

- Types of credit you’ve used: 10%

- Amount of new credit: 10%

The VantageScore model is definitely more lenient in its scoring system. People will check their VantageScore online and when they apply for credit with a lender their score can be dramatically different.

I would get many calls from consumers who had applied for credit with our bank and could not understand why the score we had was so different from the one they were seeing online. The majority of institutional lenders will only pull a FICO Score from one or all of the three reporting bureaus depending on the type of credit you are applying for.

Why Do I Have Three Different FICO Scores?

In addition to the FICO and VantageScore which we have already gone over, you also have a distinct and individual credit score with each of the credit reporting agencies. Equifax, Experian, and TransUnion may not be getting all of your payment information. Your credit score will be similar between each of these agencies. But some lenders do not report to all three bureaus or they may have misreported information. This is important to note because you may be denied if a lender only pulls from one reporting bureau and the information is not correct.

You may have noticed this on your own credit report. My husband paid off his truck in 2020. Equifax showed the loan as having been paid off, Experian did not show the truck at all and TransUnion didn’t update the information showing he paid it off. Now that debt still appears on his TransUnion credit report. His TransUnion score will not reflect that loan being paid off.

In addition, FICO itself has several different scores it offers based on the type of credit applied for.

Can I See My FICO Credit Scores For Free?

I was excited to see that FICO and the banks are making these changes. You can now see your free FICO score from all three credit bureaus depending on which banks hold your accounts. FICO itself charges $19.95 a month for you to see those scores. They also throw in full copies of your credit reports. The banks typically do not offer that.

Every month I can go on to two of the credit card accounts I have and see my free FICO Credit score due to the FICO Score Open Access Program. But it is only from one reporting bureau so I am not seeing all three scores and I am not seeing the accounts on my credit report.

FICO Score Open Access is a program that helps educate consumers on FICO Scores and increases consumer access to FICO Scores. FICO works with over 200 financial institutions to give their customers absolutely free access to the FICO Scores they use to manage credit accounts.